May 04, 2022.

Oceanic Finance

The ubiquity of nautical terminology in the financial lexicon is quite fascinating when you actually think about it. Perhaps it has something to do with the ancient nexus between high finance and maritime trade? Think the Dutch East India Company – the first to be listed on the Amsterdam Stock Exchange, the world’s first bourse – an earth-shaking financial innovation, founded way back in 1602. Or perhaps it has something to do with the uncanny resemblance that stock price charts have with ocean waves?

The ebb and flow of liquidity can roil global financial markets. A tsunami of foreign capital floods into emerging markets, turning them upside down. It is the venerable Warren Buffet who observed that you only discover who’s been swimming naked when the tide flows out, to colourfully illustrate consequences to leveraged positions when financial tides recede. Financial markets are usually overvalued when awash with cash. Surging oil prices feed waves of global inflation. Frothy markets face corrections.

Companies that require money, float securities in capital markets. Captains at the helm of industry navigate these companies through financial storms. Those that survive have their heads above water. Floundering companies are sinking ships. Rudderless ones are said to be adrift. Companies that are favoured by macroeconomic gales are advantaged by tailwinds, while those that are not are disadvantaged by headwinds. Companies that survive stay afloat, but those that do not, require a bail out.

Interestingly, super rich dudes hold their wealth in offshore tax havens located on remote islands out at sea and can’t quite resist the temptation to buy themselves a yacht to flaunt their entry into the exclusive billionaire’s club.

Zoologically speaking, successful investors are big fish while super successful ones are sharks. These marine similes explain why the popular American business reality television series is called Shark Tank – episodes feature entrepreneurs pitching their fledgling companies to a set of sharks who decide whether to buy equity in these companies.

But the unforgiving financial ocean out there is teeming with a multitude of species. By implication, the entrepreneur who is selling his company must therefore be a sardine if the buyers are indeed sharks. But again, it was the venerable Warren Buffet who warned us lesser human beings to beware of entrepreneurs selling IPOs – after all, only suckers sell money printers on the cheap.

Sardines

In one of the episodes first aired on 13-Nov-2015[1], the sharks were Mark Cuban, Kevin O’Leary, Robert Herjavec, Lori Greiner and Daymond John. Jeff Overall, the entrepreneur who had founded a start-up called PolarPro, successfully sold 20% of the company to the sharks for $1m thus valuing the company at $5m. This financially titillating 10-minute episode can be viewed here https://www.youtube.com/watch?v=rWOduv5VsuM. PolarPro produces and sells camera accessories, and was founded in 2011 when revenues were a mere $8K and rose to $2.8m by 2014 representing a CAGR of 333%. The company is not leveraged

[1] https://en.wikipedia.org/wiki/List_of_Shark_Tank_episodes

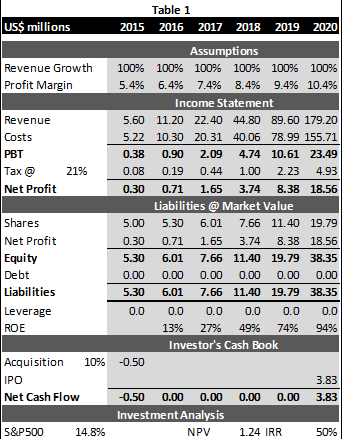

Jeff expects revenues to grow 100% to $5.6m in 2015 with a net profit of $300K and expects to continue revenue growth at 100% for the next 2-3 years given his forecast that they would reach $40-50m in that time span. This seems reasonable given his track record and with some thoughtful imagination it is possible to construct the Income Statement forecast in Table 1 which conforms to all points discussed in the episode. Additionally, we assume conservatively that Net Profit Margin will increase 1% per annum because of increasing economies of scale and a quick descent down the learning curve, both resulting from rapid growth. US corporate tax rates are at 21%[1].

Jeff starts out wanting to sell 10% for US$500K. Therefore, even if the investor exits via a conservatively priced IPO in 2020 the forecasted IRR is 50% which is 3.4 times the S&P500 average return at 14.8%[2] and provides a fat margin of safety to accommodate forecasting risks. In other words, PolarPro is the proverbial goose that lays golden eggs. Aesop’s fables provide us with ample warning about the demerits of selling such a goose.

Kevin O’Leary backed out of this juicy deal of a lifetime without even making an offer because he feared impending copycat competition but Jeff spends aggressively on R&D, holds 8 patents and has hitherto successfully kept copycats at bay. Aesop should also have warned us about the demerits of failing to buy such a golden goose.

Sharks???

Bidding starts with Mark Cuban offering $500K for 10% which is exactly Jeff Overall’s ask.

Then Daymond John offers PolarPro his expertise in product delivery and licensing plus $500K for 15%. This is very unlike a shark. After all, Jeff Overall is not likely to accept this offer which is vastly inferior to Mark Cuban’s, especially since PolarPro has hitherto been delivering superlative results without any external expertise in product delivery and licensing.

Next, Lori Greiner also offers $500K for 10% but ups the ante against Mark Cuban by offering her marketing expertise to PolarPro as a sweetener. This is also unlike a shark. After all, this is hardly a better offer than Mark Cuban’s since PolarPro seems to have been delivering 24-carat golden eggs anyway, without any external marketing expertise.

Lastly, Robert Herjavec partners with Mark Cuban to offer $1m for 20% which values PolarPro at $5m. At which point Mr. Rip Van Winkle a.k.a. Daymond John, finally wakes up to offer $1m for 17.5% which values PolarPro at $5.7m but is rejected by Jeff Overall – why partner with an un-shark even if the offer is better?

Ultimately, the Robert Herjavec-Mark Cuban consortium clinches the deal at $1m for 20%. Jeff Overall is thrilled that he succeeded in selling 20% instead of 10% of his golden goose and by his demeanour would have sold an even greater slice had he received an offer. Sardines, like leopards, never change their spots!

Great Whites

Out there in the deep ocean frolics a Hollywood superstar immortalized in the blockbuster film “Jaws” – the one and only great white shark. Interestingly, this fearsome predator, the sultan of sharks, has never been successfully held captive in any man-made shark tank[3] and is found only in the wild. Unsurprisingly, this indomitable species was absent in the episode.

[1] https://en.wikipedia.org/wiki/Corporate_tax_in_the_United_States

[2] https://www.fool.com/investing/how-to-invest/stocks/average-stock-market-return/

[3] https://en.wikipedia.org/wiki/Great_white_shark

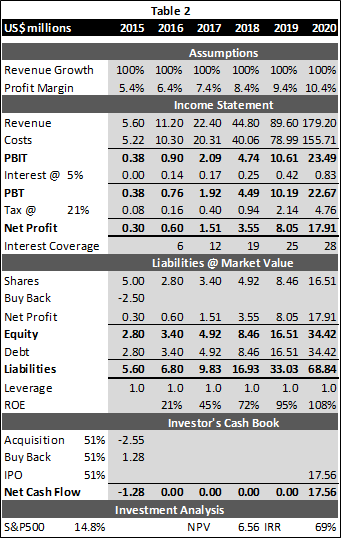

Its Wall Street avatar, no less a formidable predator, would have instantly sniffed a killing when its calculating financial brain recognized that PolarPro’s unleveraged ROE at a minimum of 13% in 2016 is 2.6 times the US 10-year BBB corporate bond yield trading at around 5% in 2015[1]. This great white shark would have offered to buy 51% of PolarPro for $2.55m thus still valuing PolarPro at $5m, while standing ready to loosen purse strings even further in the unlikely event that Jeff Overall resists the sale of 51%.

Why 51%? Because controlling interest facilitates a board resolution to change financing policy unopposed, to leverage PolarPro by borrowing $2.8m and simultaneously returning $2.5m to shareholders by way of buyback. Effectively this great white shark would have successfully taken over 51% of this golden goose for a mere $1.28m, given that it would have regained $1.28m of its $2.55m acquisition price through the buyback, more or less immediately. Why would it have regained $1.28m? Because of its 51% share of the $2.5m buyback.

The change in capital structure, leads to a highly reasonable debt-equity ratio for PolarPro of 1.0 for a company in the pinkest of financial health. Interestingly, there is virtually no default risk since we have a minimum interest coverage of 6 in 2016 rising to 28 in 2020 as shown in Table 2.

Therefore, the forecasted IRR is 69% which is a mouth-watering 4.7 times the S&P500 average return at 14.8% and provides a very comforting margin of safety to accommodate forecasting risks. Importantly, it beats the 50% unleveraged IRR by a whopping 19% and is 1.38 times the unleveraged option. This goose lays golden eggs that are 38% bigger. Great white sharks, like sardines and leopards, never change their spots!

Incidentally, Jeff Overall is absolutely ecstatic because he receives an immediate $1.125m in buybacks in addition to the $2.55m acquisition price leaving him with $3.675m cash in hand – never doubt the golden hands of an enthusiastic serial entrepreneur.

Back to the Future

But out there beneath the waves are great whites and great whites and some are smarter than the rest. It seems, smart great whites masquerade as sardines – camouflage is a competitive advantage in the art of war.

At the beginning of 2022, PolarPro’s actual net worth is US$15m[2] having been valued by sharks at US$5m at the end of 2015 – so in reality PolarPro generated an IRR of 24.6%. Nevertheless, this is 1.66 times the S&P500 average return at 14.8%. This goose laid golden eggs that were 66% bigger. Warren Buffet is still dean of Wall Street.

[1] https://www.raymondjames.com/-/media/rj/dotcom/files/wealth-management/market-commentary-and-insights/bond-market-commentary/tfi_chartbook.ashx?la=en