Impact of latent variables in option trading on GILT segment (A working Paper)

By

Bikramaditya Ghosh

Backdrop

GILT as a segment (especially the 10 Year one) is always a coveted one for all types of treasury related activities, across countries. GILT is traditionally purchased and traded either as future segment or in cash segment. Traditionally in India GILT trading happens more on the futures route. Ideally this depends upon the number of contracts on offer and open interest generated among traders from various treasuries. Trading in GILT Options predominantly happens in Banks, and it’s both calculations as well as perception based. If post opting for a certain option the caller backs out, then he has to pay the necessary premium as a cost. Most of the time either the Options in GILT segment do not gets exercised.

Literature Review

The most apt paper in this domain was written by Jayant Verma (1996) in IJAF. This paper has argued that the most practical and sensible way of valuing interest rate options in India is to use a single factor lattice based model. Single factor models (which are based on the short term interest rate) are to be preferred not only for their greater simplicity, but also because multi-factor models would require knowledge of the dynamics of long term rates which is not available in India at present. Within the class of single factor lattice based models, the Black-Derman-Toy model emerged as the most serious contender because its assumptions are consistent with the behaviour of interest rates in India as documented in Verma (1996).

Objective

Objective of this study lies in detection of predictors in Option trading in GILT segment in India. Traditionally it has been noticed that number of contracts and open interest determines the volume of GILT Options. It is important to mention here that DTBs are excluded here as a segment deliberately as their coupons are not specific and floating in nature.

Methodology

This study is used on the base on a unique Gaussian Mixture Model platform, called “Panel Data Regression”. Two sets of heavily traded underlying assets make the dependent variables a minimum of two. Bond Options for last year has been used for finding out the impact of latent variables. Two premier segments Bond options were taken in to consideration. The reason being , more than 80% of the trading in GILT Options for past 365 calendar days happened in these two counters. They are 8.40% GS 2024 and 8.83% GS 2023. Same underlying assets are taken into consideration. Total Volume should ideally depend upon number of contracts (namely X1 variable) and open interest (namely X2 variable) but as two layers of underlying assets are there so Panel Data Regression has been utilized. Two dummy variables (namely d1 and d2) will represent two different layers of underlying assets. These d1 and d2 could be special central bank events such as rate cut or hike; it could also be hike in sentiment as GDP or IIP numbers go north. This could also result from the idea of increase in foreign assets in the country. Total numbers of observations are 295. Out of which 195 belongs to 8.40% GS 2024 and 100 belongs to 8.83% GS 2023.

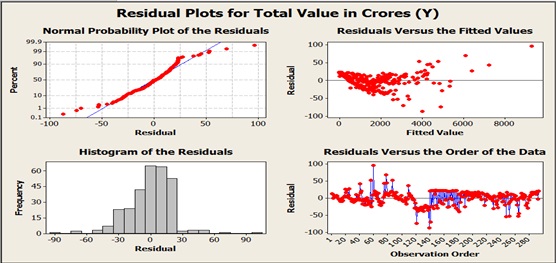

Results

Post Panel Data Regression with 95% confidence level, the researcher found that,

* d2 is highly correlated with other X variables

* d2 has been removed from the equation.

The regression equation is

Total Value in Crores (Y) = – 37.3 + 0.0206 Total Contracts (X1) + 0.000139 Open Interest (X2) + 0.00124 d1

Output

Predictor Coeff SE T P Occurrence (%)

Constant -37.258 3.311 -11.25 0.000 NA

Total Contracts (X1) 0.0206 0.00002 898.77 0.000 100%

Open Interest (X2) 0.00014 0.00001 12.21 0.000 100%

d1 0.00124 0.0003 3.52 0.001 100%

S = 20.7430 R² = 100.0% R² (Adj) = 100.0%

Interpretation

[1] As a coefficient d1 has more impact over the option volume beating open interest.

[2] Total number of contracts, Open Interest and d1 impact the Volume of GILT Options to a great extent i.e. 100%.

[3] Adjusted R² proves the solidity of this model.

[4] d1 proves the presence of a dominant latent variable.

[5] 15 outliers has been spotted in the first Option contract (underlying asset 8.40% GS 2024) compared to 4 in the second Option contract (underlying asset 8.83% GS 2023).

[6] Latent variable d1 has more impact on the Option contract with underlying asset 8.40% GS 2024.

[7] d1 would almost surely be an event based (change in GDP, IIP, RBI Rate, Foreign Currency Reserve etc.) parameter, so it is hinting towards an sentiment or confidence based X variable.

[8] d2 is either mixed with X1 or mixed with X2 , as found

in Panel Data Analysis; that means it could be a sub set of either number of contracts, or Open Interest or both at the same time.

in Panel Data Analysis; that means it could be a sub set of either number of contracts, or Open Interest or both at the same time.

Further scope of study

[1] Identifying and decoding the latent variable d1.

[2] Continuing the similar work for a much larger time frame to get more accuracy.

Citations

[1] Brooks, C., & Oozeer, M. C. (2002). Modeling the implied volatility of options on long gilt futures. Journal of Business Finance & Accounting, 29(1‐2), 111-137.

[2] Fung, W., & Hsieh, D. A. (2001). The risk in hedge fund strategies: Theory and evidence from trend followers. Review of Financial studies, 14(2), 313-341.

[3] Tompkins, R. G. (2001). Implied volatility surfaces: uncovering regularities for options on financial futures. The European Journal of Finance, 7(3), 198-230.